Our 7th consumer data report is being released this morning exclusively to you.

For months now, we have seen consumers buying for “need” vs. “want”. The most recent data shows that this has completely solidified. The average American has increasing anxiety over the economy and is cutting their family budget — hoarding their money, not spending it.

Our methodology since March has included 29,263 survey respondents, scaled to 200+ million US consumers in our database, 550 million+ connected devices, and tracking 10 billion+ online decisions every day.

I can’t emphasize this enough — if you want to know what’s happening in the economy, before your competitors, then you must pay attention to this new data we are putting out to you for free today.

First, the semi-good news:

We are seeing angst around the health risks from the Coronavirus subside slightly. Our data clearly shows that online grocery orders are down and a growing number of consumers have returned to shopping at physical grocery stores.

Also, we are now seeing 43% of American consumers dining-in at a restaurant once a week. The stimulus and the weather have been huge boosts to the VERY fragile restaurant industry.

The big worry for the restaurant industry is how bad will it get when the weather turns cold, outdoor dining ends, and/or when the government puts us in another coronavirus lockdown. I’m still bearish on the restaurant industry collapsing by at least 25%, but the government checks and warm weather has held off this disruption temporarily.

Now, the bad news:

While American consumers are more accepting of the coronavirus health risks, there is a deep concern around the fragility of the overall economy. Consumer confidence remained high until June but has dissipated every month since. In our current study, this includes:

- 69.9% of American consumers think the current quality of the U.S. economy is “poor” or “very poor.” Another 20% of Americans think it’s just “fair.” Only 10.1% of Americans think the quality of our economy is “good” or “excellent.”

- 73% of Americans believe our economy will not return to normal before at least the spring of 2021.

- Consumers that believe their personal and work life will “never return to normal” has increased by 26% since June (In June, I wrote about how this number was a huge economic indicator. You can read it HERE).

When it comes to consumers buying for “need-only” instead of “wants and desires” — check out what our data says:

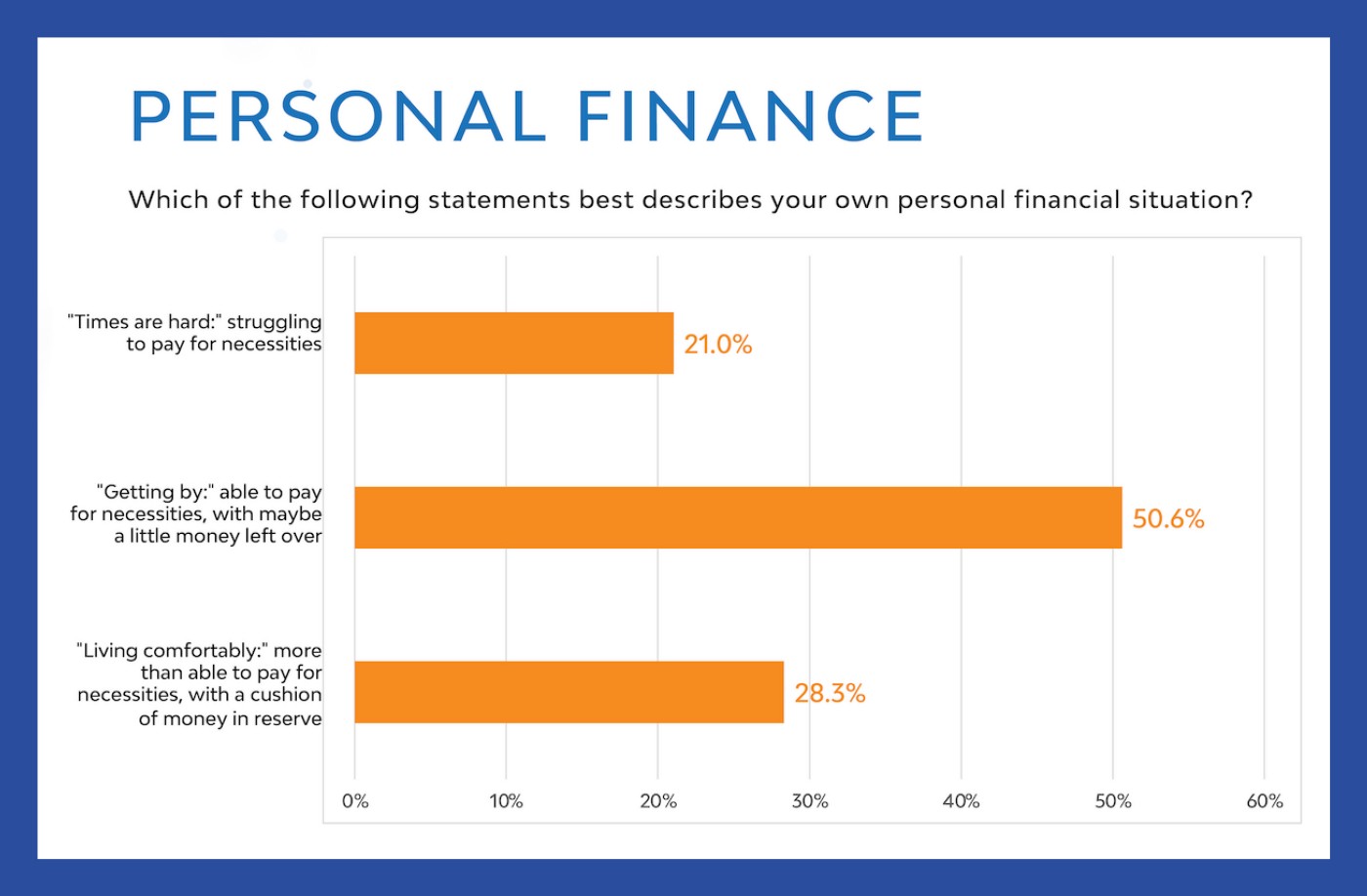

- Regarding the personal finances of the American consumer, 71.6% are “struggling to pay for necessities” or just “getting by.” The remaining 28.3% of Americans feel like they are “living comfortably” which is indicative of the consumers benefiting from sustained wealth, new business growth, the rising stock market, etc.

- 82.4% of Americans are worried about their family’s financial situation.

- 41.9% of Americans have INCREASED their focus on monitoring and budgeting family expenses. This is a key indicator on buying for “need” only.

How have these “need” indicators negatively impacted certain sectors? Check this out:

- While we’ve seen an increase in Americans returning to physical locations like grocery stores and general merchandise stores (buying for need), like Walmart, Target, Costco, there has been a precipitous drop in consumers returning to clothing retail and electronic stores. Along with the restaurant industry and the commercial real estate industry, expect massive disruptions with these specific sectors.

- Only 7.5% of American consumers indicate they will make some major purchases in the next 90 days (i.e. automobiles, appliances, etc.)

- 95.5% of consumers will not purchase a luxury item (i.e. fine jewelry, designer clothing, etc.) in the next 90 days. *We’ve tracked this number since early June and it has trended in the wrong direction every single month.

What can you take from this new data to save or grow a business?

Two trends are popping through the data that will absolutely benefit your business in these uncertain times.

- To repeat — you must communicate (through your marketing) that your product or service is an essential “need” for the consumer. For example, one of our clients is a huge regional furniture store. Their marketing is focused on the importance of clean and new furniture in this uncertain health moment + offering great discounts and sales right now. This particular client had two of the best months in their history (this summer) — even though our data clearly states most consumers aren’t making “major purchases” right now. How is that possible in such a “need” vs. “want” economy? It was done by following the data and properly messaged ads focusing on the needs of their customers (which we found to be “safety” and “discounts”).

- You must quickly eliminate “friction-to-transaction” for your customer/client. All consumers (including seniors) have solidly moved to purchasing in the online marketplace. According to Compuware, “A single bad experience on a website, makes users 88% less likely to visit the website again.” Customers/client’s ability to purchase your products or services must be made as easy as possible. Any barrier to the transaction will most likely be a lost customer forever. Let me give you an example of what I’m talking about. We recently met with a food producer that is only serving the B2B market (grocery stores, wholesalers, etc.). But, this innovative business owner has realized that he must quickly adapt to the eCommerce world and sell his popular food online. It’s a big shift but the goal is to adapt and reduce-the-friction to transaction for the consumer.

I am giving you FREE access to all of our surveys (March, April, May, June, July, and August + our two surveys analyzing the protest culture on consumers) — just go to winbigmedia.com and click on the “Covid-19 Consumer Research” tab — my analysis of all the data is also found on this page.

PS — If you know a business owner or marketer that will benefit from these key insights (and get an advantage over their competition), forward this article and/or data to them so they can use it in this critical moment. And when they subscribe to my exclusive bi-weekly data insights, they will always get first access to the data before any of their competition.